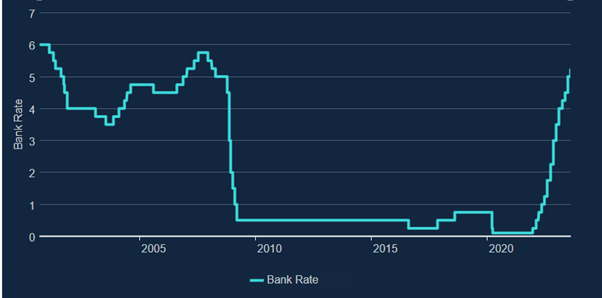

For the fourteenth consecutive time in a row, the Bank of England has raised interest rates in order to try to reduce inflation. Now at 5.25%, interest rates are at the highest they’ve been for fifteen years, however the base rate was only raised a quarter point yesterday, as opposed to the half point rise that we saw last month.

What is the Relationship Between Interest Rates and Inflation?

We have often seen governments increase interest rates in an attempt to curb inflation as the higher the interest rate, the more expensive the cost of borrowing is. This encourages the nation to save their money and not spend, which in turn means there is less demand for products forcing providers to drop their prices.

What Does This Mean for Debt?

Unfortunately, for those who are looking to borrow or who have variable rate loans and mortgages, the Bank of England announcement will have been discouraging news. This is because those on variable rate mortgages usually see an immediate rise in their monthly payments. If you have any concerns about this rise and would like to know what it means to you, please contact your Adviser.

What Does This Mean for Savings?

The current high period of interest rates has given our clients an opportunity to finally increase growth on their cash savings with some banks offering rates of 5%. We at MPA have catered to this increased demand by now offering a ‘cash Savings platform’ to our clients (read more here). Additionally, annuities are now becoming a more favourable option to some due to rising rates after having declining popularity in recent years.

What Can We Expect for the Future?

Many people believe that this will not be the last interest rise of this year, with investment specialist Hymans Robertson stating they expect interest rates to “peak of c6.0% in UK” with an inflation rate of “4.6% for end [of] 2023”.